Why Mule Accounts Are Increasing

The rise of digital banking, instant payments, online scams, and remote account opening has created new opportunities for criminals to move illicit funds quickly and anonymously. Fraudsters increasingly recruit individuals through social media, fake job offers, investment schemes, and romance scams to gain access to bank accounts for money laundering and fraud activities. As financial transactions become faster and more interconnected across borders, mule accounts have become a key tool for concealing the source and destination of illegal funds. This growing trend has made mule account detection a major priority for banks, fintech companies, and AML compliance teams worldwide.

Understanding Mule Accounts: Definition and Overview

Mule accounts have become a growing concern for banks, fintech companies, and financial institutions worldwide. As digital payments and online banking continue to expand, criminals are increasingly using mule accounts to move illicit funds and conceal financial crime activities.

A mule account is a bank account that is used to receive, transfer, or withdraw money obtained through illegal activities. The individual operating the account, often called a money mule, may knowingly participate in criminal schemes or may be unaware that they are helping fraudsters move illicit funds.

Criminals use mule accounts to support activities such as money laundering, scam payments, cybercrime, and other forms of financial fraud. By transferring money through multiple accounts, they make it more difficult for financial institutions and law enforcement agencies to trace the origin of the funds.

For banks and fintech companies, mule accounts present significant challenges. They can contribute to financial losses, regulatory risks, AML compliance issues, and reputational damage. As a result, identifying and preventing mule account activity has become an important part of modern fraud detection and financial crime prevention strategies.

Understanding how mule accounts operate is the first step toward strengthening transaction monitoring, customer screening, and risk management processes. With financial crime becoming increasingly sophisticated, organizations need proactive approaches to detect suspicious account behavior and reduce exposure to fraud and money laundering risks.

How the Money Mule Network Works

Money mule networks help criminals move illicit funds through multiplaccounts to hide the source of the money and avoid detection. These transactions are often made to look legitimate, making it harder for financial institutions to identify suspicious activity.

1. Recruitment and Account Creation

The process usually begins when fraudsters recruit individuals through fake job offers, social media, investment opportunities, or other scams. The recruited person may be asked to open a new bank account or provide access to an existing one.

2. Account Verification and Setup

Before using the account, fraudsters may collect additional information such as identity documents, banking credentials, or mobile numbers. This helps them gain greater control over the account and prepare it for future transactions.

3. Account Warm-Up

To make the account appear legitimate, fraudsters often conduct small transactions over a period of time. This “warm-up” phase helps build trust and reduces the likelihood of larger transactions being flagged immediately.

4. Money Transfer

Once the account appears trustworthy, stolen or illicit funds are transferred into the mule account. The money may come from fraud victims, scam operations, cybercrime activities, or money laundering schemes.

5. Layering and Fund Movement

The funds are quickly moved through multiple accounts, payment platforms, or jurisdictions. This layering process makes it more difficult to trace the original source of the money.

6. Cash Withdrawal or Conversion

In the final stage, the funds are withdrawn through ATMs, transferred to other bank accounts, or converted into cryptocurrency. Criminals often prefer cryptocurrency because it can provide additional anonymity and make investigations more challenging.

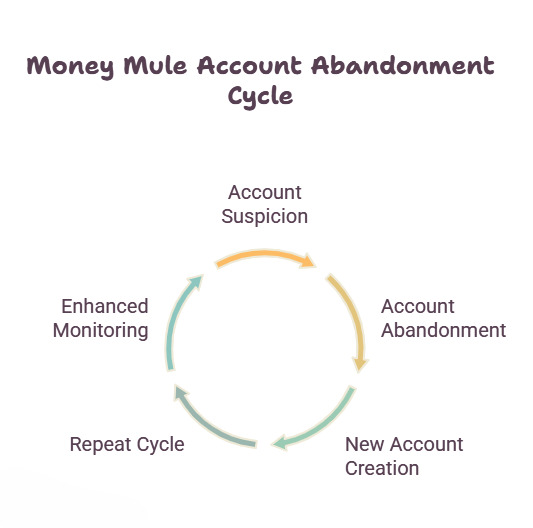

7. Account Abandonment

Once the account becomes suspicious or attracts attention from financial institutions, criminals may stop using it and move to a new mule account, repeating the cycle with other recruited individuals.

Understanding how money mule networks operate helps banks, fintech companies, and compliance teams identify suspicious behaviors earlier and strengthen their fraud detection and AML monitoring programs.

Types of Mule Accounts

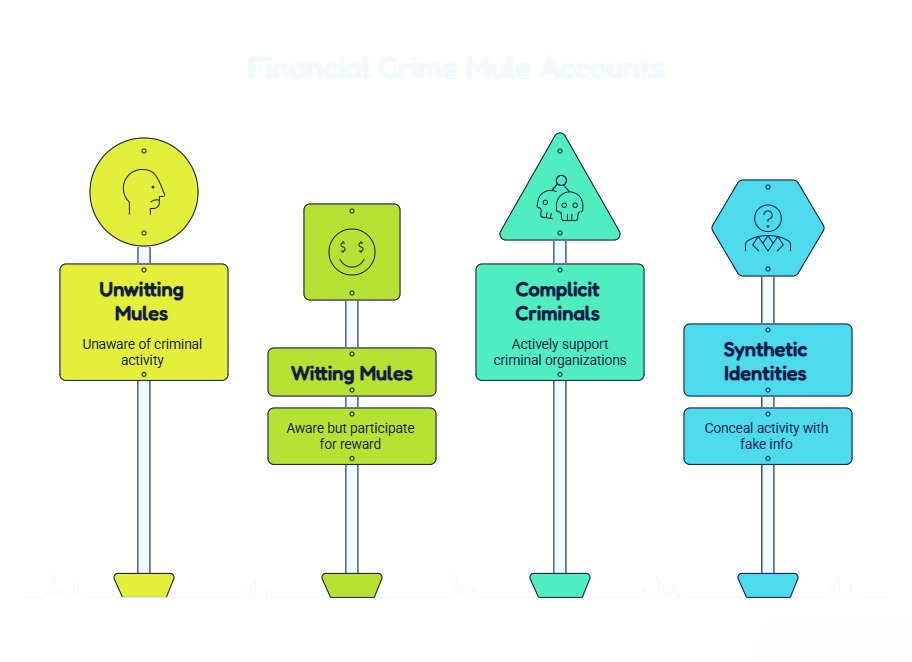

Unwitting Mules

Unwitting mules are individuals who unknowingly become involved in financial crime. They may respond to fake job offers, online opportunities, or requests from people they trust, without realizing their accounts are being used to move illicit funds.

Witting Mules

Witting mules are aware that the activity may be suspicious but choose to participate in exchange for financial rewards. They knowingly help transfer funds on behalf of fraudsters or criminal networks.

Complicit Criminal Mules

Complicit criminal mules actively work with criminal organizations to support money laundering and fraud schemes. They often manage multiple accounts and play a direct role in moving illegal funds through the financial system.

Synthetic Identity Mule Accounts

Synthetic identity mule accounts are created using a combination of real and fabricated personal information. These accounts appear legitimate but are designed to conceal criminal activity, making them difficult for financial institutions to detect and trace.

Identifying Red Flags of Mule Account Activity

Detecting mule accounts early is essential for preventing financial fraud, money laundering, and other financial crimes. While mule accounts can appear legitimate, certain behaviors and transaction patterns may indicate elevated risk.

Some common red flags include:

- Sudden increases in account activity that do not match the customer’s typical behavior.

- Large incoming payments followed by immediate transfers or withdrawals.

- Frequent transactions involving multiple unrelated individuals or accounts.

- Dormant accounts becoming unexpectedly active and processing significant transaction volumes.

- Funds moving rapidly through the account with little or no clear business or personal purpose.

- Multiple accounts linked to the same device, phone number, IP address, or beneficiary.

- Transactions involving high-risk locations or jurisdictions without a reasonable explanation.

- Customers who are unable to explain the purpose of unusual transactions or account activity.

While a single indicator may not confirm mule account activity, multiple red flags occurring together can signal increased financial crime risk. Continuous transaction monitoring, customer screening, and behavioral analysis can help financial institutions identify suspicious activity more effectively and strengthen AML and fraud prevention efforts.

How Mule Accounts Support Financial Crime

Mule accounts play a critical role in helping criminals move and conceal illicit funds. Common financial crimes supported by mule accounts include:

- Money Laundering: Criminals transfer funds through multiple accounts to hide their origin and make tracing more difficult.

- Authorized Push Payment (APP) Fraud: Victims are tricked into sending money to accounts controlled by fraudsters, which are often mule accounts.

- Scam Proceeds Movement: Funds generated from investment scams, romance scams, and impersonation fraud are frequently moved through mule account networks.

- Terrorist Financing: In some cases, mule accounts may be used to transfer funds linked to terrorism-related activities while appearing legitimate.

- Cross-Border Financial Crime: Criminal organizations use mule accounts to move money across countries, making investigations and regulatory oversight more challenging.

By facilitating the movement of illicit funds, mule accounts remain a significant concern for financial institutions and AML compliance teams.

How Banks and Fintech Companies Detect Mule Accounts

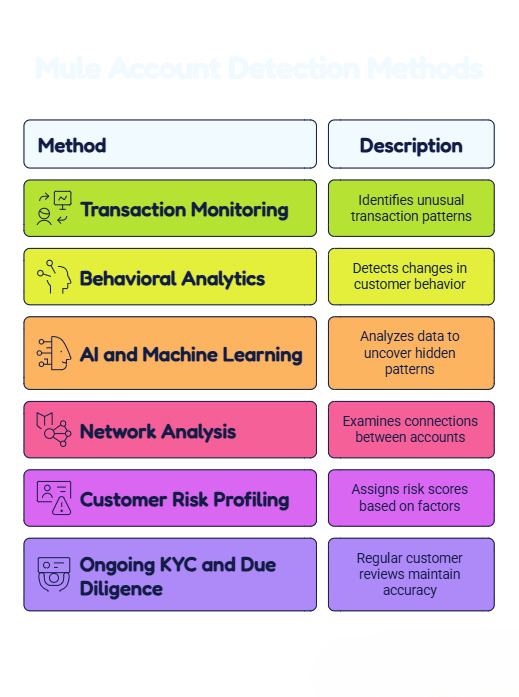

Financial institutions use multiple techniques to identify mule account activity and reduce financial crime risks. Common detection methods include:

- Transaction Monitoring: Identifies unusual transaction patterns, such as rapid fund transfers, multiple incoming payments followed by immediate withdrawals, or activity involving high-risk jurisdictions.

- Behavioral Analytics: Detects changes in customer behavior that may indicate suspicious activity, such as sudden increases in transaction volumes.

- AI and Machine Learning: Analyzes large amounts of data to uncover hidden patterns, identify emerging fraud risks, and improve detection accuracy.

- Network Analysis: Examines connections between accounts, devices, and individuals to identify organized criminal networks.

- Customer Risk Profiling: Assigns risk scores based on customer behavior, geographic exposure, and other risk factors to support enhanced monitoring.

- Ongoing KYC and Due Diligence: Regular customer reviews help maintain accurate information, identify new risks, and strengthen AML compliance efforts.

By combining these approaches, banks and fintech companies can detect mule accounts more effectively and prevent financial fraud before significant losses occur

The Role of Technology in Mule Account Detection

As financial crime becomes more sophisticated, technology plays a critical role in helping banks and fintech companies detect mule account activity more effectively. Key technologies include:

- Real-Time Monitoring: Detects suspicious transactions as they occur, enabling faster intervention and reducing potential financial losses.

- Risk Scoring: Evaluates customers and transactions using multiple risk indicators, helping compliance teams prioritize investigations.

- Behavioral Intelligence: Analyzes customer behavior and transaction patterns to identify unusual activities that may indicate mule account usage.

- Automated Investigations: Streamlines alert reviews and case management by automatically gathering relevant information and highlighting risk factors.

- AI-Driven Anomaly Detection: Uses artificial intelligence to identify unusual patterns and emerging fraud schemes that traditional rule-based systems may miss.

By combining these technologies, financial institutions can strengthen mule account detection, improve AML compliance, and enhance overall fraud prevention efforts.

How Users Can Avoid Mule Account Fraud

Individuals can reduce the risk of becoming involved in mule account fraud by staying alert to common warning signs and following basic security practices:

- Avoid “Easy Money” Offers: Be cautious of job advertisements or online opportunities that promise quick earnings for receiving or transferring money.

- Never Share Bank Account Access: Do not provide your banking credentials, debit cards, OTPs, or account access to anyone.

- Verify Employment Opportunities: Research companies and employers before accepting remote jobs that involve handling payments or transferring funds.

- Be Cautious of Online Relationships: Fraudsters often use romance scams and social media connections to recruit money mules.

- Question Unusual Payment Requests: If someone asks you to receive money and forward it to another account, it may be part of a money laundering scheme.

- Monitor Account Activity: Regularly review bank statements and transaction history for unauthorized or suspicious activity.

- Report Suspicious Requests: Contact your bank immediately if you receive unusual payment instructions or suspect fraudulent activity.

Understanding these risks can help individuals protect themselves from becoming money mules and prevent their accounts from being used in financial crime.

How IDYC360 Can Help Strengthen Mule Account Detection

IDYC360 helps financial institutions strengthen mule account detection through an integrated approach to AML compliance, fraud prevention, and risk management. Key capabilities include:

- Customer Screening: Identifies high-risk individuals and entities during onboarding and throughout the customer lifecycle.

- Risk Assessment: Evaluates customer risk levels using multiple risk indicators to support informed decision-making.

- Transaction Monitoring: Detects suspicious transactions, unusual payment patterns, and potential mule account activity.

- AML Compliance Support: Helps organizations enhance customer due diligence, monitoring, and compliance processes.

- Fraud Detection: Combines AML controls and fraud detection capabilities to identify financial crime risks more effectively.

- Continuous Monitoring: Tracks changes in customer behavior and emerging risks over time.

- Regulatory Readiness: Supports organizations in meeting evolving regulatory and compliance requirements.

Future Trends in Mule Account Detection

As financial crime evolves, technology will play an increasingly important role in mule account detection. Key trends include:

- AI-Powered Fraud Prevention: Using artificial intelligence to detect suspicious behavior and emerging fraud patterns.

- Network Intelligence: Identifying connections between customers, accounts, devices, and transactions to uncover criminal networks.

- Real-Time Compliance Monitoring: Enabling faster detection and response to potential financial crime risks.

- Predictive Risk Analytics: Anticipating emerging threats before they develop into significant fraud or money laundering events.

Conclusion

Mule accounts are a key enabler of modern financial crime, supporting activities such as money laundering, APP fraud, cybercrime, and cross-border criminal operations. For banks, fintech companies, and payment providers, the challenge extends beyond identifying suspicious accounts to understanding the networks and behaviors behind them.

Effective mule account detection requires a combination of transaction monitoring, behavioral analytics, customer risk assessment, network analysis, and ongoing AML compliance measures. While traditional rule-based systems remain important, advanced technologies such as AI, machine learning, and real-time monitoring are increasingly essential for identifying evolving threats.

Organizations that adopt integrated AML and fraud prevention strategies are better equipped to reduce risk, strengthen compliance, and protect customers and institutions from financial crime. As financial crime continues to evolve, proactive mule account detection will remain a critical component of effective financial crime prevention.

Frequently Asked Questions

1. What is a mule account?

A mule account is a bank account used to receive, transfer, or move funds derived from criminal activities, often on behalf of fraudsters or criminal organizations.

2. What is a money mule?

A money mule is an individual who transfers or moves illegally obtained funds through their bank account, either knowingly or unknowingly.

3. How do banks detect mule accounts?

Banks use transaction monitoring, behavioral analytics, AI models, network analysis, customer screening, and ongoing monitoring to identify suspicious account activity.

4. Why are mule accounts dangerous?

Mule accounts help criminals launder money, facilitate fraud schemes, conceal illicit funds, and support broader financial crime activities.

5. Can someone become a money mule unknowingly?

Yes. Many individuals are recruited through fake jobs, social media scams, investment schemes, or romance scams without realizing they are participating in criminal activity.

Ready to Stay

Compliant—Without Slowing Down?

Move at crypto speed without losing sight of your regulatory obligations.

With IDYC360, you can scale securely, onboard instantly, and monitor risk in real time—without the friction.

Related to this topic:

Common Fraud Detection Rules Used by Banks and Fintechs