Financial fraud continues to evolve as criminals adopt increasingly sophisticated methods to exploit digital banking, payment systems, and financial platforms. To combat these threats, banks and fintech companies rely on fraud detection systems that can identify suspicious activities before they result in financial losses.

One of the most effective and widely used approaches is rule-based fraud detection. These systems use predefined rules and thresholds to monitor transactions, user behavior, and account activity in real time. When a transaction or action matches a predefined risk condition, an alert is generated for further investigation.

This article explores some of the most common fraud detection rules used by banks and fintechs and explains why they remain an essential component of modern fraud prevention strategies.

What Is Fraud Detection?

Fraud detection is the process of identifying, monitoring, and preventing fraudulent activities across applications, digital platforms, transactions, and customer accounts. It uses a combination of rules, analytics, artificial intelligence, and behavioral monitoring to detect suspicious patterns, unusual activities, or potential financial crimes before they cause significant harm.

By continuously analyzing transaction data and customer behavior, fraud detection systems can identify risks such as account takeover, identity theft, payment fraud, money laundering, and mule account activity. These systems help organizations respond quickly to threats, reduce financial losses, and protect both customers and business operations.

Effective fraud detection is essential for banks, fintechs, payment providers, and other regulated organizations. Beyond preventing fraud, it supports AML/CFT compliance, strengthens risk management, enhances customer trust, and helps maintain the security and integrity of financial systems in an increasingly digital environment.

Common Types of Fintech Fraud

As digital financial services continue to grow, fraudsters are developing increasingly sophisticated methods to exploit vulnerabilities. Understanding the most common types of fintech fraud can help organizations strengthen their fraud prevention strategies and protect customers from financial loss.

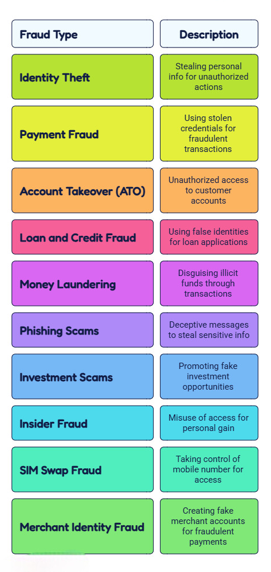

Identity Theft

Fraudsters steal personal information to open accounts, access financial services, or conduct unauthorized transactions in another person’s name.

Payment Fraud

Criminals use stolen payment credentials, compromised cards, or unauthorized access to payment accounts to complete fraudulent transactions.

Account Takeover (ATO)

Attackers gain unauthorized access to customer accounts using stolen credentials obtained through phishing, social engineering, or data breaches.

Loan and Credit Fraud

Fraudsters use false or stolen identities to apply for loans or credit products, often leaving financial institutions with significant losses.

Money Laundering

Illicit funds are transferred through multiple accounts or transactions to disguise their origin and integrate them into the legitimate financial system.

Phishing Scams

Cybercriminals use deceptive emails, messages, or websites that imitate trusted organizations to steal sensitive information such as passwords and financial details.

Investment Scams

Fraudsters promote fake or misleading investment opportunities, often promising unrealistic returns to attract victims and obtain their funds.

Insider Fraud

Employees or trusted insiders misuse their access to systems, customer data, or financial resources for personal gain or criminal purposes.

SIM Swap Fraud

Criminals take control of a victim’s mobile number to intercept authentication codes, enabling unauthorized access to financial accounts.

Merchant Identity Fraud

Fraudsters create fake merchant accounts or impersonate legitimate businesses to process fraudulent payments and facilitate financial crime.

Effective fraud prevention requires continuous monitoring, risk-based controls, identity verification, transaction screening, and advanced fraud detection technologies to identify and mitigate these threats before they cause significant damage.

Importance of Fraud Detection Systems

Fraud detection systems play a vital role in protecting organizations, customers, and financial ecosystems from increasingly sophisticated financial crimes. Fraudulent activities can result in significant financial losses, operational disruptions, regulatory penalties, and long-term reputational damage. As digital transactions continue to grow, effective fraud detection has become a critical component of risk management and business security.

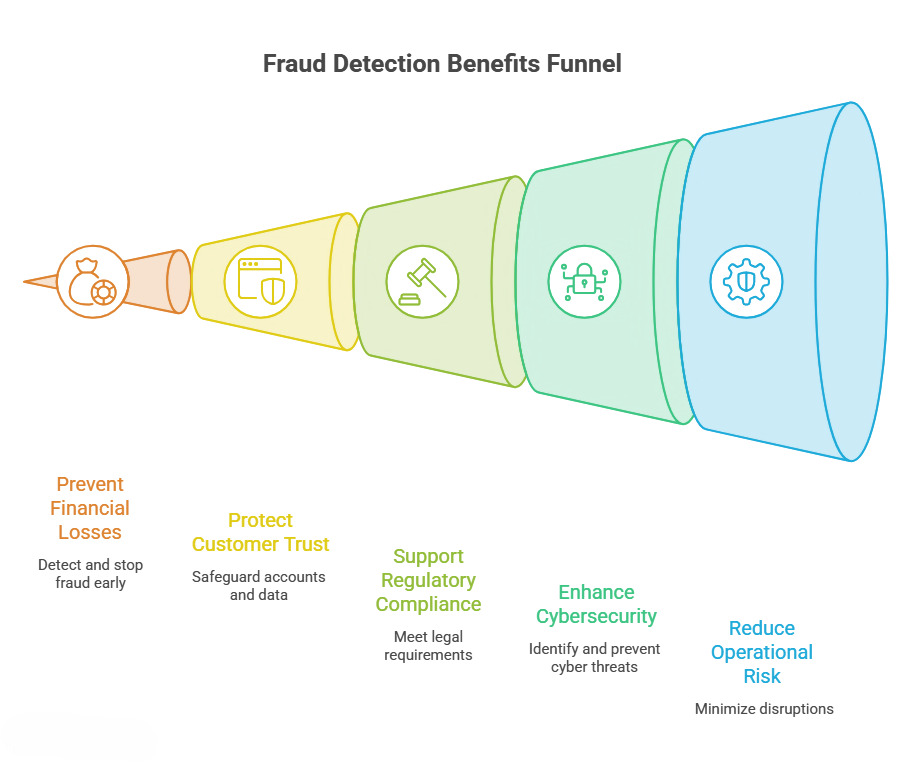

Key benefits of fraud detection systems include:

- Preventing Financial Losses: Detects suspicious activities early, helping organizations stop fraudulent transactions before losses occur.

- Protecting Customer Trust: Strengthens customer confidence by safeguarding accounts, personal information, and financial assets.

- Supporting Regulatory Compliance: Helps organizations meet AML/CFT, KYC, sanctions screening, and other regulatory requirements while reducing the risk of penalties and enforcement actions.

- Enhancing Cybersecurity: Identifies unauthorized access attempts, account takeovers, phishing attacks, and other cyber-enabled fraud threats.

- Reducing Operational Risk: Minimizes disruptions caused by fraud investigations, chargebacks, and financial disputes.

- Improving Risk Management: Provides greater visibility into suspicious activities, enabling organizations to make informed risk-based decisions.

- Protecting Brand Reputation: Prevents incidents that could damage an organization’s credibility, customer relationships, and market position.

- Enabling Real-Time Monitoring: Continuously analyzes transactions and customer behavior to identify potential threats as they occur.

- Reducing False Positives: Modern fraud detection solutions help organizations focus on genuine risks while improving operational efficiency.

- Supporting Business Growth: Creates a secure environment that enables organizations to expand digital services with greater confidence.

In today’s rapidly evolving threat landscape, fraud detection systems are no longer optional. They are an essential defense mechanism that helps organizations protect assets, maintain compliance, strengthen customer relationships, and ensure the integrity of financial operations.

Challenges in Fraud Detection

As fraud detection technologies continue to improve, fraudsters are constantly evolving their tactics to bypass security controls. Modern criminals use social engineering, stolen credentials, automation, and even AI-powered techniques to mimic legitimate user behavior, making fraud increasingly difficult to identify.

One of the biggest challenges is the growing volume of data generated by digital transactions. Organizations must analyze vast amounts of information in real time to detect suspicious activities without impacting operational performance.

Another common challenge is the high number of false positives. Traditional rule-based systems may flag legitimate transactions as suspicious, creating additional workloads for fraud teams and increasing investigation costs. At the same time, organizations must ensure genuine fraud cases are not overlooked.

Businesses also face the challenge of balancing security with customer experience. While measures such as multi-factor authentication, account verification, and transaction monitoring help reduce fraud, excessive security controls can create friction for legitimate users and negatively impact customer satisfaction.

To address these challenges, organizations increasingly adopt advanced fraud detection solutions that combine rule-based monitoring, behavioral analytics, artificial intelligence, and risk-based decision-making to improve detection accuracy while maintaining a seamless user experience.

Common Fraud Detection Rules Used by Banks and Fintechs

Banks and fintech companies rely on rule-based fraud detection systems to identify suspicious activities and reduce the risk of financial crime. These rules monitor transactions, customer behavior, and account activity in real time, generating alerts when predefined risk conditions are met.

Some of the most common fraud detection rules include:

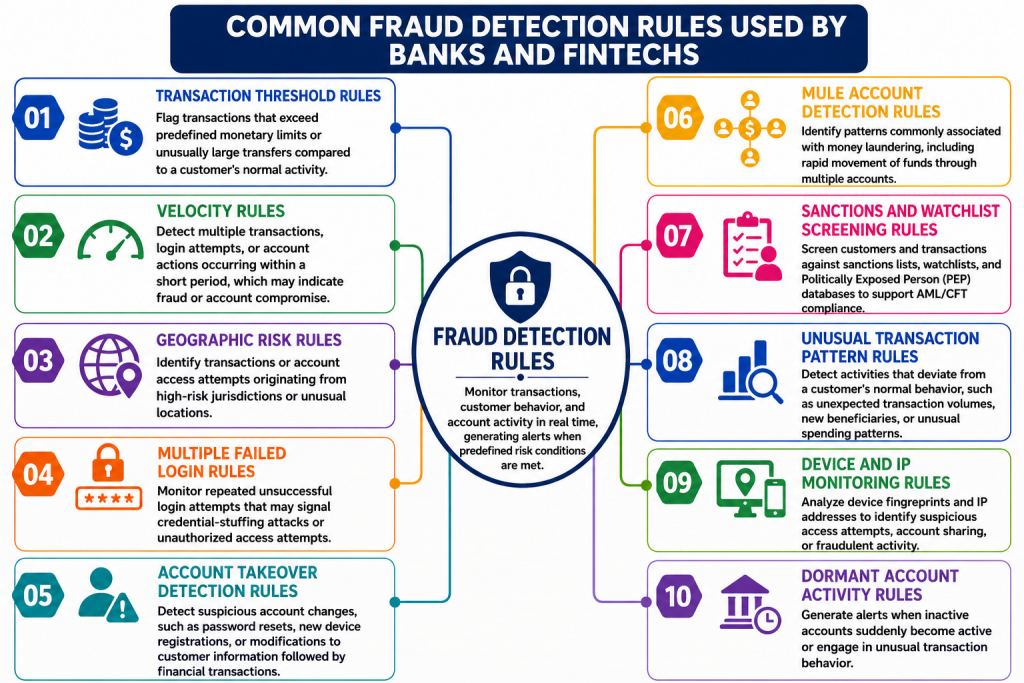

Transaction Threshold Rules

Flag transactions that exceed predefined monetary limits or unusually large transfers compared to a customer’s normal activity.

Velocity Rules

Detect multiple transactions, login attempts, or account actions occurring within a short period, which may indicate fraud or account compromise.

Geographic Risk Rules

Identify transactions or account access attempts originating from high-risk jurisdictions or unusual locations.

Multiple Failed Login Rules

Monitor repeated unsuccessful login attempts that may signal credential-stuffing attacks or unauthorized access attempts.

Account Takeover Detection Rules

Detect suspicious account changes, such as password resets, new device registrations, or modifications to customer information followed by financial transactions.

Mule Account Detection Rules

Identify patterns commonly associated with money laundering, including rapid movement of funds through multiple accounts.

Sanctions and Watchlist Screening Rules

Screen customers and transactions against sanctions lists, watchlists, and Politically Exposed Person (PEP) databases to support AML/CFT compliance.

Unusual Transaction Pattern Rules

Detect activities that deviate from a customer’s normal behavior, such as unexpected transaction volumes, new beneficiaries, or unusual spending patterns.

Device and IP Monitoring Rules

Analyze device fingerprints and IP addresses to identify suspicious access attempts, account sharing, or fraudulent activity.

Dormant Account Activity Rules

Generate alerts when inactive accounts suddenly become active or engage in unusual transaction behavior.

By implementing these fraud detection rules, banks and fintechs can identify suspicious activities more effectively, reduce financial losses, strengthen AML/CFT compliance, and protect both customers and business operations from emerging fraud threats.

How IDYC360 Helps Strengthen Fraud Detection

As fraud schemes become more sophisticated, organizations require a proactive and intelligence-driven approach to fraud prevention. Traditional monitoring methods alone are often insufficient to detect emerging threats, complex fraud networks, and rapidly evolving financial crime patterns.

IDYC360 provides a comprehensive fraud detection and risk management platform designed to help banks, fintechs, payment providers, and regulated businesses identify suspicious activities in real time. By combining rule-based monitoring, risk-based controls, behavioral analysis, and AML-focused compliance capabilities, organizations can strengthen their defenses against financial crime while improving operational efficiency.

Key capabilities include:

- Real-Time Transaction Monitoring to identify suspicious activities as they occur.

- Configurable Risk Rules that enable organizations to adapt controls based on business requirements and emerging threats.

- AML/CFT Compliance Support through risk-based monitoring and investigative workflows.

- Customer Risk Assessment to help identify high-risk individuals, accounts, and transaction patterns.

- Alert Management and Case Investigation tools that streamline fraud reviews and reduce response times.

- Data-Driven Insights that support informed decision-making and continuous risk optimization.

By helping organizations detect fraud earlier, reduce operational risk, and strengthen compliance programs, IDYC360 enables businesses to protect customers, safeguard financial assets, and maintain trust in an increasingly complex digital environment.

Conclusion

Fraud detection remains a critical priority for banks, fintechs, and financial institutions operating in today’s digital economy. From identity theft and account takeover fraud to money laundering and payment fraud, organizations face a wide range of threats that require continuous monitoring and effective risk controls.

Rule-based fraud detection continues to serve as a foundational defense mechanism, helping organizations identify suspicious activities, support regulatory compliance, and protect customers from financial harm. However, as fraud tactics evolve, organizations must combine traditional monitoring approaches with advanced analytics, behavioral intelligence, and risk-based decision-making.

By implementing comprehensive fraud detection strategies and leveraging solutions such as IDYC360, organizations can strengthen fraud prevention efforts, improve compliance outcomes, and build a more secure and trusted financial ecosystem.

Frequently Asked Questions (FAQs)

What is fraud detection?

Fraud detection is the process of identifying, monitoring, and preventing suspicious activities that may indicate financial crime. It helps organizations detect risks such as identity theft, payment fraud, account takeover, and money laundering before significant damage occurs.

Why is fraud detection important for banks and fintechs?

Fraud detection helps financial institutions reduce financial losses, protect customer accounts, maintain regulatory compliance, and strengthen trust in digital financial services.

What are fraud detection rules?

Fraud detection rules are predefined conditions used to identify suspicious activities. When a transaction or user action matches a specific risk criterion, the system generates an alert for further review.

What are the most common fraud detection rules used by banks and fintechs?

Common fraud detection rules include transaction threshold monitoring, velocity checks, geographic risk monitoring, account takeover detection, sanctions screening, mule account detection, device monitoring, and unusual transaction pattern analysis.

What is Account Takeover (ATO) fraud?

Account Takeover (ATO) fraud occurs when criminals gain unauthorized access to a customer’s account using stolen credentials, phishing attacks, social engineering, or data obtained from breaches.

Ready to Stay

Compliant—Without Slowing Down?

Move at crypto speed without losing sight of your regulatory obligations.

With IDYC360, you can scale securely, onboard instantly, and monitor risk in real time—without the friction.

Related to this topic: