Financial fraud is one of the most pressing threats to businesses, governments, and individuals worldwide. From investment scams to identity theft and money laundering, fraud undermines the integrity of financial systems and causes billions of dollars in losses each year.

As digital transactions continue to grow, fraudsters are using increasingly sophisticated methods to exploit financial systems. Organizations must therefore adopt strong fraud prevention and detection measures to protect their operations, customers, and reputation.

For compliance teams, financial fraud is not just a legal issue but a major component of fraud risk management and financial crime prevention. This article explains what financial fraud is, explores common schemes, and provides best practices for preventing fraud in a global business environment.

What Is Financial Fraud?

At its core, financial fraud involves using deception or misrepresentation for unlawful financial gain. Fraudsters manipulate systems, falsify information, or abuse trusted relationships to exploit victims. It can take many forms, ranging from corporate embezzlement and payment fraud to identity theft and cross-border investment scams.

Financial fraud affects both organizations and individuals, often resulting in financial losses, reputational damage, regulatory penalties, and reduced customer trust. As financial services become increasingly digital, fraud schemes are evolving in complexity, making early detection and prevention more important than ever.

Regulators classify financial fraud as part of broader financial crime, alongside money laundering, bribery, and terrorist financing. Effective anti-money laundering compliance frameworks often overlap with fraud prevention measures, since both aim to safeguard the integrity of the financial system and protect businesses from emerging risks.

Common Types of Financial Fraud

Below are some of the most common types of financial fraud affecting individuals, businesses, and financial institutions:

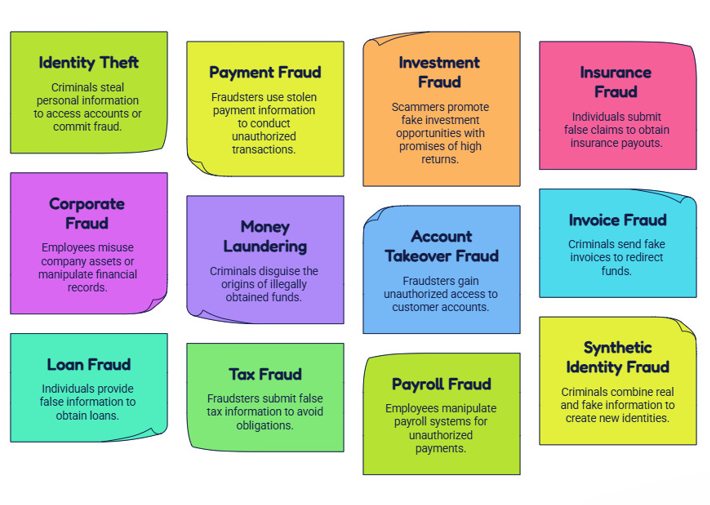

Identity Theft: Criminals steal personal information, such as bank account details, government-issued IDs, or login credentials, to access accounts or commit fraud.

Payment Fraud: Fraudsters use stolen payment information or compromised accounts to conduct unauthorized transactions.

Investment Fraud: Scammers promote fake investment opportunities with promises of high returns and low risk, often resulting in significant financial losses for victims.

Insurance Fraud: Individuals or groups submit false claims, exaggerate damages, or provide misleading information to obtain insurance payouts.

Corporate Fraud: Employees, executives, or third parties misuse company assets, manipulate financial records, or embezzle funds for personal gain.

Money Laundering: Criminals attempt to disguise the origins of illegally obtained funds by moving them through legitimate financial systems and transactions.

Account Takeover Fraud: Fraudsters gain unauthorized access to customer accounts and use them to transfer funds, make purchases, or steal sensitive information.

Invoice Fraud: Criminals send fake invoices or alter payment details on legitimate invoices to redirect funds to fraudulent accounts.

Loan Fraud: Individuals provide false information or forged documents to obtain loans or credit they would not otherwise qualify for.

Tax Fraud: Fraudsters submit false tax information, claim fraudulent refunds, or conceal income to avoid tax obligations.

Payroll Fraud: Employees manipulate payroll systems, submit false expense claims, or create fake employees to receive unauthorized payments.

Synthetic Identity Fraud: Criminals combine real and fake personal information to create new identities that can be used to open accounts and commit financial crimes.

As financial fraud continues to evolve, organizations must strengthen their fraud detection, customer verification, and transaction monitoring processes to identify suspicious activity and reduce risk.

Why Does Financial Fraud Happen?

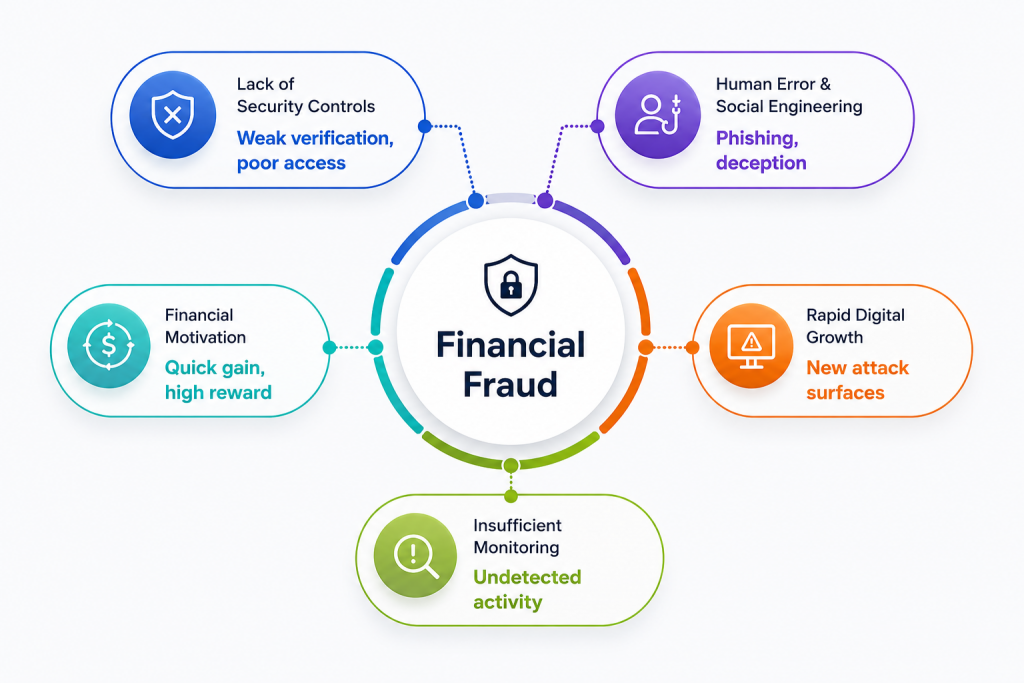

Financial fraud occurs when criminals identify opportunities to exploit weaknesses in people, processes, or technology for financial gain. As digital transactions and online services continue to expand, fraudsters have more ways to target individuals and organizations.

Some of the most common reasons financial fraud occurs include:

Lack of Security Controls: Weak verification processes, poor access controls, and outdated security systems can make it easier for fraudsters to succeed.

Human Error and Social Engineering: Fraudsters often manipulate people through phishing emails, fake websites, or deceptive communications to gain access to sensitive information.

Rapid Digital Growth: The increasing use of online banking, digital payments, and remote services has created new opportunities for cyber-enabled fraud.

Insufficient Monitoring: Organizations that lack effective transaction monitoring and fraud detection systems may struggle to identify suspicious activities in time.

Financial Motivation: Many fraud schemes are driven by the desire for quick financial gain, making individuals and businesses attractive targets.

Emerging Fraud Trends in 2026

Recent fraud cases highlight how quickly financial crime is evolving in the digital age. In 2026, organizations and consumers have faced a growing number of AI-powered scams, phishing attacks, investment fraud schemes, and account takeover incidents. Fraudsters are increasingly using advanced technologies such as deepfake voices, synthetic identities, and social engineering tactics to deceive victims and bypass traditional security controls.

Authorities have also reported a rise in online investment scams, business email compromise (BEC) attacks, and cyber-enabled fraud networks that use mule accounts to move illicit funds. These cases demonstrate the importance of real-time monitoring, customer verification, and proactive fraud detection measures.

How to Protect Yourself from Financial Fraud

Protecting yourself from financial fraud requires a combination of awareness, vigilance, and strong security practices. The following measures can help reduce your risk of becoming a victim:

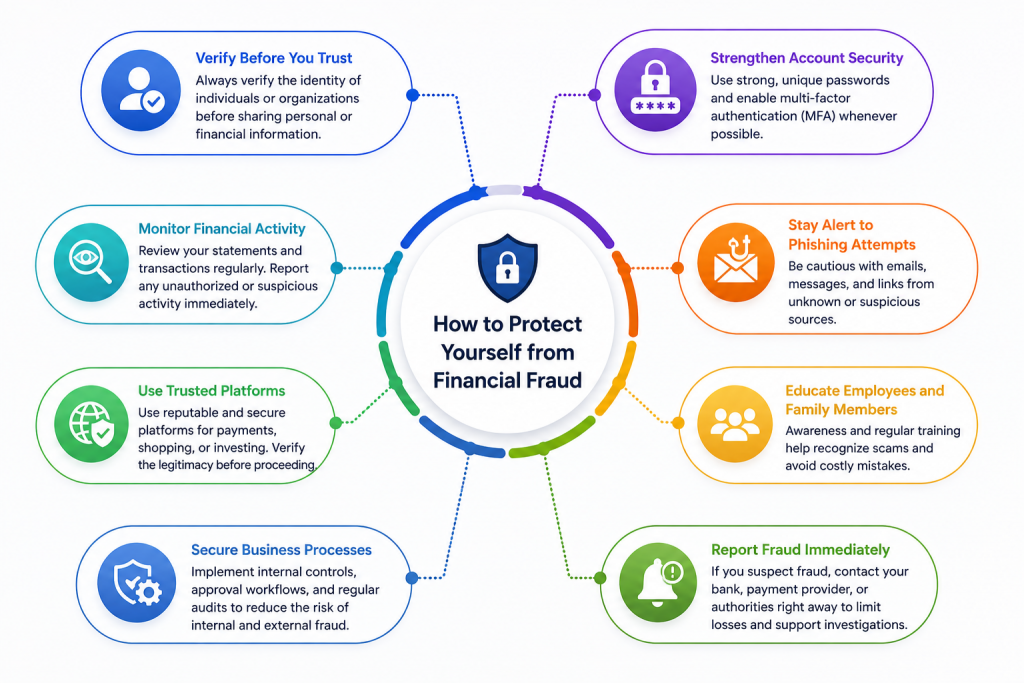

Verify Before You Trust

Always verify the identity of individuals or organizations requesting personal, financial, or account information. Use official contact details and trusted communication channels before sharing sensitive data.

Strengthen Account Security

Use strong, unique passwords for your accounts and enable multi-factor authentication (MFA) whenever possible. Regularly update devices and software to protect against cyber threats.

Monitor Financial Activity

Review bank statements, credit card transactions, and digital payment activity regularly. Promptly report any unauthorized or suspicious transactions to your financial institution.

Stay Alert to Phishing Attempts

Be cautious when opening emails, messages, or links from unknown sources. Fraudsters often impersonate trusted organizations to steal credentials or financial information.

Use Trusted Platforms

When making payments, shopping online, or investing, use reputable and secure platforms. Check website security indicators and verify the legitimacy of service providers before proceeding.

Educate Employees and Family Members

Awareness is one of the most effective defenses against fraud. Regular training can help individuals recognize common scam tactics and avoid costly mistakes.

Secure Business Processes

Organizations should implement internal controls, approval workflows, and regular audits to reduce the risk of internal and external fraud.

Report Fraud Immediately

If you suspect fraudulent activity, act quickly. Contact your bank, payment provider, or relevant authorities as soon as possible to help limit losses and support investigations.

By adopting these preventive measures, individuals and organizations can significantly reduce their exposure to financial fraud and strengthen their overall security posture.

How to Prevent Financial Fraud

Preventing financial fraud requires a proactive approach that combines strong controls, continuous monitoring, and effective risk management. Organizations must identify suspicious activities early and implement measures that reduce exposure to financial crime.

Some of the most effective fraud prevention practices include:

- Strengthen Customer Verification: Verify customer identities through robust KYC and due diligence processes to prevent identity-related fraud.

- Monitor Transactions Continuously: Use real-time transaction monitoring to detect unusual behavior and potentially fraudulent activities.

- Implement Risk-Based Screening: Screen customers, vendors, and transactions against sanctions, watchlists, and other risk indicators.

- Enhance Employee Awareness: Train employees to recognize phishing attempts, social engineering tactics, and other common fraud schemes.

- Strengthen Internal Controls: Establish clear approval processes, access controls, and regular audits to reduce internal fraud risks.

- Leverage Advanced Technology: Use AI-powered analytics and fraud detection solutions to identify emerging threats and suspicious patterns.

- Conduct Regular Risk Assessments: Continuously evaluate fraud risks and update controls to address evolving threats.

Organizations that adopt a comprehensive fraud prevention strategy are better positioned to protect their customers, maintain regulatory compliance, and reduce financial losses.

Solutions such as IDYC360 help organizations strengthen fraud prevention efforts through customer screening, transaction monitoring, risk assessment, and AML/CFT compliance capabilities, enabling businesses to detect and manage financial crime risks more effectively.

Conclusion

Financial fraud remains a significant challenge for businesses, financial institutions, and individuals worldwide. As fraud schemes become more sophisticated and technology-driven, organizations must adopt a proactive approach to fraud prevention, detection, and risk management.

Understanding the different types of financial fraud, the factors that contribute to fraud risk, and the latest fraud trends can help organizations strengthen their defenses and respond more effectively to emerging threats. By implementing robust customer verification, transaction monitoring, employee awareness programs, and risk-based controls, businesses can reduce financial losses, protect customer trust, and support regulatory compliance.

Advanced solutions such as IDYC360 further enhance these efforts by helping organizations identify suspicious activities, manage fraud risks, and strengthen AML/CFT compliance. In an increasingly digital financial landscape, a comprehensive fraud prevention strategy is essential for maintaining security, resilience, and long-term business success.

Frequently Asked Questions (FAQs)

What is financial fraud?

Financial fraud is the act of using deception, misrepresentation, or dishonest practices to obtain money, assets, or financial benefits illegally.

What are the most common types of financial fraud?

Some common types of financial fraud include identity theft, payment fraud, investment fraud, account takeover fraud, insurance fraud, money laundering, and phishing scams.

Why is financial fraud increasing?

Financial fraud is increasing due to the rapid growth of digital transactions, online banking, mobile payments, and increasingly sophisticated fraud techniques such as AI-powered scams and social engineering attacks.

How does financial fraud affect businesses?

Financial fraud can result in financial losses, reputational damage, regulatory penalties, operational disruptions, and loss of customer trust.

What are the warning signs of financial fraud?

Common warning signs include unusual transaction activity, unauthorized account access, suspicious payment requests, inconsistent customer information, and unexpected changes in user behavior.

Ready to Stay

Compliant—Without Slowing Down?

Move at crypto speed without losing sight of your regulatory obligations.

With IDYC360, you can scale securely, onboard instantly, and monitor risk in real time—without the friction.

Related to this topic:

Common Fraud Detection Rules Used by Banks and Fintechs