Introduction

Today’s fast digital world transaction volume and speed both are increasing rapidly especially UPI, mobile banking and fintech platforms. but with the growth challenges will be also come like financial fraud and money laundering

controlling these risks AML (anti-money laundering) compliance becomes a critical framework . its ensure illegal money not enter in system

In India, AML regulations fall under the Prevention of Money Laundering Act (PMLA), 2002, wherein regulators such as the Reserve Bank of India and FIU-IND play a crucial role in monitoring and enforcement.

What is AML complaints

(black money) from entering the legal financial system. This involves the necessity of banks, fintechs, and other financial institutions to authenticate their customers’ identity (KYC), transaction monitoring, and submission of suspicious activities. In India, the AML process is regulated by Prevention of Money Laundering Act, 2002. Here, RBI and FIU-India play an important role.

Like:- If a new account is made at a bank where the customer creates an account using false papers and makes several large transactions in a very short span, this gets flagged by the AML process because this is out of the norm. The account is immediately flagged by the bank and a Suspicious Transaction Report (STR) is sent to FIU-India.

In short, it makes the financial system safe from any type of fraud and money laundering practices.

Why AML compliance is important

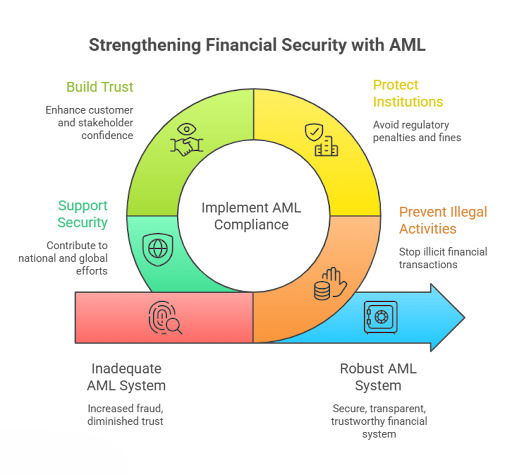

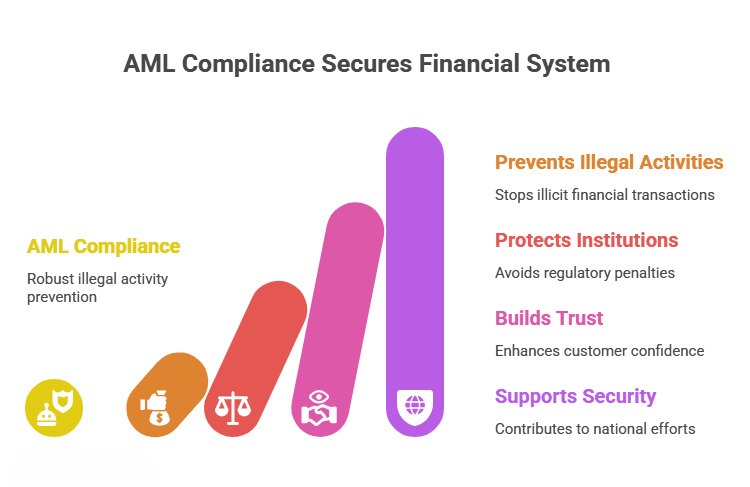

AML (Anti-Money Laundering) compliance is crucial for making the financial system secure, transparent, and trustworthy. In today’s digital era where online transactions and fintech are growing rapidly AML compliance provides a robust mechanism for preventing illegal activities.

- Prevents illegal financial activities

- Protects institutions from regulatory penalties

- Builds trust with customers and stakeholders

- Supports national and global security efforts

If a proper AML system is not in place, fraud within a bank or company may increase, public trust diminishes, and they may face legal repercussions.

Key AML Regulations in India

- Prevent of money laundering act 2002

This is the primary legislation that defines money laundering offenses and outlines penalties.

- Reserve Bank of India (RBI) Guidelines

Reserve Bank of India issues KYC and AML guidelines for banks and financial institutions.

- Financial Intelligence Unit (FIU-IND)

Financial Intelligence Unit India is responsible for collecting and analyzing financial transaction reports and sharing intelligence with enforcement agencies.

Key Component of AML Compliance

- Know your customer (KYC)

Customer identification and verification is the first step in AML compliance. Institutions must verify identity documents and assess customer risk.

- Customer Due Diligence (CDD)

Ongoing monitoring of customer activities to identify unusual or suspicious behavior.

- Transaction Monitoring

Real-time monitoring systems help detect suspicious transactions and flag anomalies.

- Suspicious Transaction Reporting (STR)

Organizations must report suspicious activities to the Financial Intelligence Unit – India.

- Record Keeping

Maintaining transaction records for a specified period as per regulatory requirements.

AML Compliance Process in India

AML compliance is a step by step process through which financial institutions detect and prevent illegal activities.

-

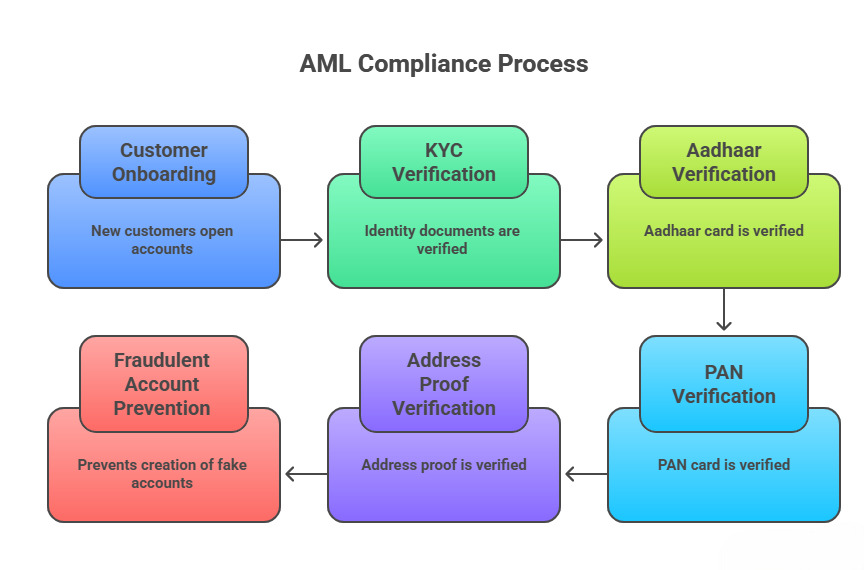

Customer Onboarding with KYC Verification

When any new customer opens their account to verify their identity KYC (know your customer) In this process, Aadhaar, PAN, and address proof are verified to ensure that fraudulent or fake accounts are not created.

-

Risk Assessment and Classification

Every customer is assigned a risk level.

- Low risk (normal users)

- Medium risk

- High risk (suspicious or high-value users)

Based on this, the bank determines the extent of monitoring required for each customer.

-

Continuous Transaction Monitoring

tracking every transaction of a customer by using a transaction monitoring system. If any unusual activity happens ( like suddenly high amount transfer) then the system generates an alert.

-

Detection of Suspicious Activities

If the system or the bank determines that a transaction deviates from normal behavior, it is considered suspicious.

- Frequent large transactions

- Logins from different locations

- Dealings with unknown accounts

-

Reporting to Financial Intelligence Unit – India

If any activity appears suspicious, the bank sends a report regarding it to the FIU-IND (STR – Suspicious Transaction Report).

The FIU-IND then conducts a further investigation.

-

Audit and Compliance Review

Regular audits are conducted to verify whether the rules are being followed properly.

If any gaps are identified, they are addressed and improved upon

Challenges in AML Compliance

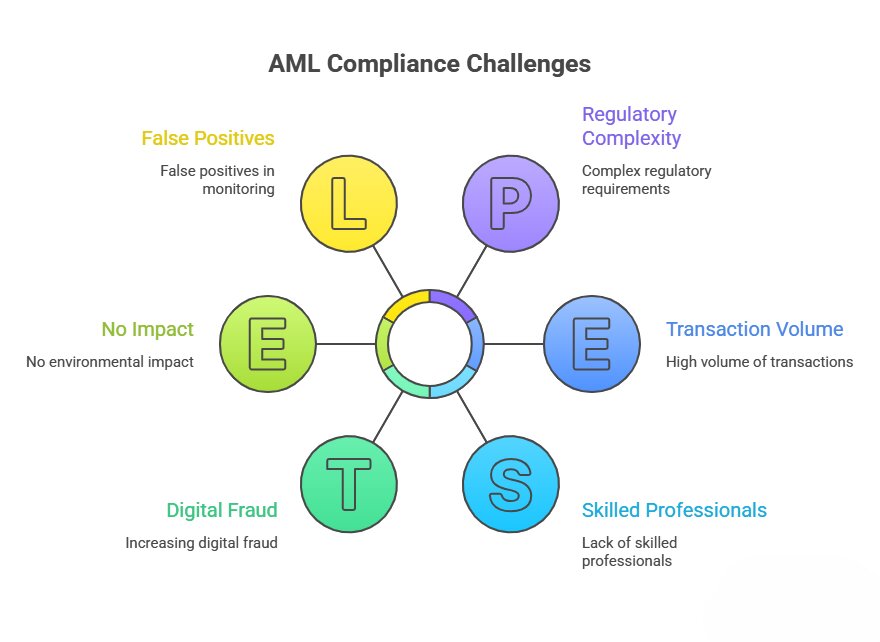

implementing AML compliance is not easy. financial institute facing to much challenges for this

- Increasing Digital Fraud and Cybercrime

Now online fraud is growing very fast, phishing, scam calls, fake apps, mule accounts, etc.

- Criminals using new techniques so detect them is so difficult

- System need to continuously update

- Complex Regulatory Requirements

In India AML rules are very strict and detailed like the Prevention of Money Laundering Act, 2002.

- Every institute has follow multiple rule and guidence

- rules will be change on time to time Which makes maintaining compliance complex

- High Volume of Transactions

Banks and fintech platforms regularly process millions of transection

- In such a large data challenging the identify suspicious activity

- for real time monitoring needed strong infrastructure system

-

False Positives in Monitoring Systems

Sometimes, the system flags even normal transactions as suspicious.

- because of this generate unnecessary alert

- The Compliance team’s time is wasted.

- Genuine customers face inconvenience.

-

Lack of Skilled Compliance Professionals

AML compliance requires trained and experienced professionals.

- There is a shortage of skilled experts in the market.

- As a result, companies face difficulties in proper monitoring and reporting.

Role of Technology in AML Compliance

Modern AML solutions use AI and machine learning to enhance detection capabilities. These systems can:

- Analyze large volumes of data in real-time

- Detect hidden patterns and anomalies

- Reduce false positives

- Improve regulatory reporting accuracy

AML Compliance for Businesses (IDYC360 Perspective)

For businesses such as IDYC360 with respect to AML compliance, regulations are only part of the process. Proactive risk management is one of the advantages of utilizing artificial intelligence (AI) for fraud detection, live monitoring, and intelligent alert systems to help prevent financial crime but also to provide an easy and seamless customer experience.

Conclusion

India’s financial situation is very dangerous because money laundering is on the rise, even though the Prevention of Money Laundering Act, 2002, and the Reserve Bank of India and Finance Intelligence Unit – India are keeping a close eye on it. In light of this, companies need to put in place the right compliance frameworks. As financial crimes become more complicated, businesses can stay in line with AML rules and provide a safe and open financial network by using advanced technologies.

Frequently Asked Questions

1. What is AML Compliance?

AML(Anti-Money Laundering) Compliance is a set of regulations and processes that help prevent illegal money from entering the financial system. It includes customer verification, transaction monitoring, and reporting suspicious activities.

2. Which law governs AML Compliance in India?

AML compliance in India is governed by the Prevention of Money Laundering Act, 2002, which defines rules and penalties related to money laundering.

3. What is the main objective of AML Compliance?

The main objective is to detect and prevent money laundering, financial fraud, and terrorist financing.

4. Why is KYC important in AML Compliance?

KYC (Know Your Customer) helps verify the identity of customers, preventing fake accounts and reducing the risk of fraud.

Ready to Stay

Compliant—Without Slowing Down?

Move at crypto speed without losing sight of your regulatory obligations.

With IDYC360, you can scale securely, onboard instantly, and monitor risk in real time—without the friction.

Related to this topic:

Common Fraud Detection Rules Used by Banks and Fintechs