Introduction

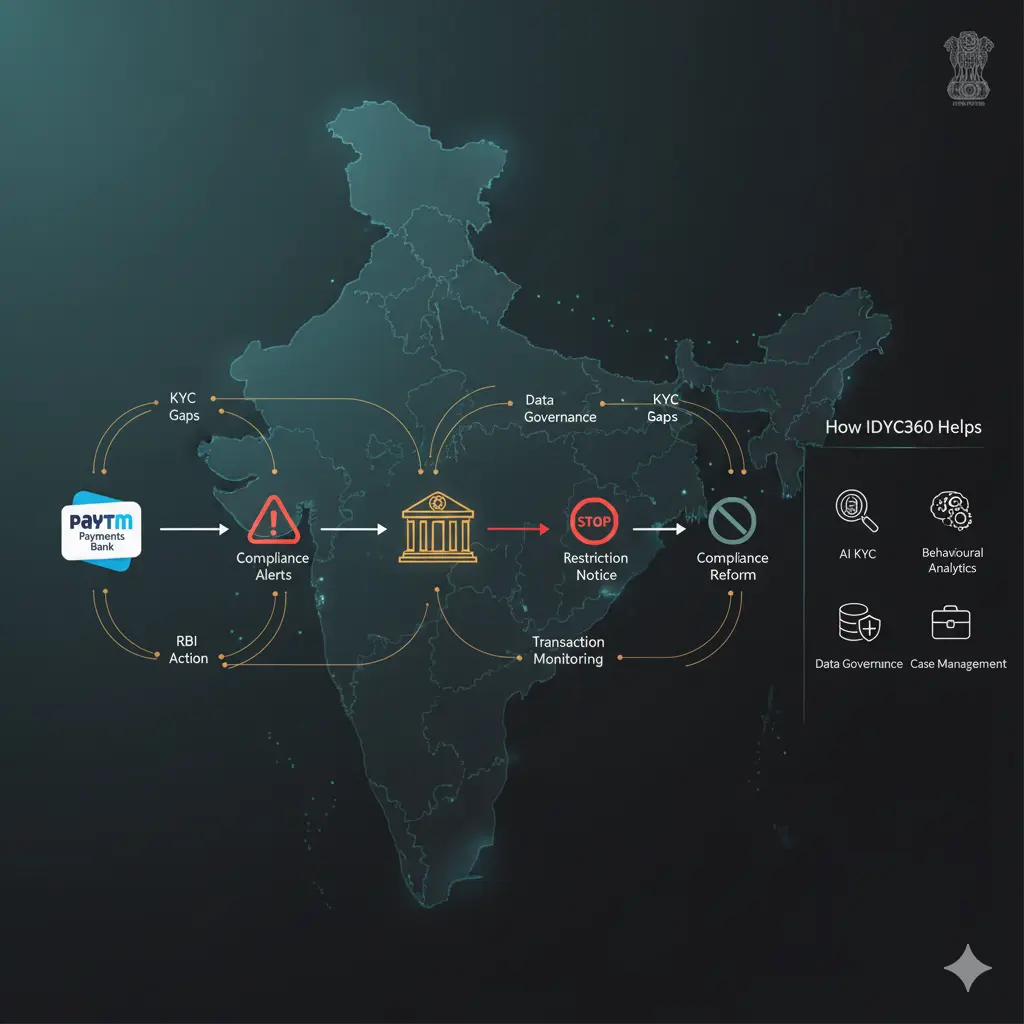

In 2024, the Reserve Bank of India (RBI) took one of its most decisive regulatory actions in recent fintech history, directing Paytm Payments Bank (PPBL) to halt onboarding new customers and later restricting most of its operations.

The decision sent shockwaves through India’s digital finance ecosystem.

For a sector that thrives on speed, scale, and innovation, RBI’s message was unmistakable: compliance is not optional; it’s existential.

This case exemplifies a growing reality in India’s fintech landscape: rapid technological growth must be matched by robust AML/CFT governance, data controls, and KYC discipline.

The episode underscores why institutions, especially digital-first financial entities, need real-time compliance intelligence systems like IDYC360 to detect weaknesses before they attract regulatory action.

Background: Rise and Regulatory Scrutiny

The Rise

Paytm Payments Bank was launched in 2017 as a digital-first banking institution designed to promote financial inclusion.

With millions of wallet users transitioning to bank accounts, PPBL became a major channel for digital deposits, merchant payments, and UPI transactions.

By 2022, the bank claimed over 330 million wallet accounts and 100 million KYC customers, positioning itself as a major node in India’s payments infrastructure.

The Scrutiny

However, with exponential growth came compliance fragility. In March 2022, the RBI first restricted PPBL from onboarding new customers due to “material supervisory concerns.” Despite subsequent remediation efforts, issues persisted.

In January 2024, the RBI escalated its response, imposing severe restrictions on account operations, citing persistent non-compliance and supervisory lapses.

The bank was asked to cease accepting new deposits and conducting credit transactions on February 29, 2024.

Anatomy of the Compliance Lapses

The RBI’s investigation revealed a constellation of operational, governance, and AML-related weaknesses.

Though detailed findings remain confidential, multiple regulatory and industry sources highlight three primary areas of concern:

KYC and Customer Due Diligence Deficiencies

- Incomplete or inconsistent KYC records across millions of accounts.

- Duplicate accounts and identity mismatches, some linked to high-risk profiles.

- Insufficient Ongoing Due Diligence (ODD) and periodic updates for existing customers.

In essence, PPBL’s rapid onboarding and API-driven integrations outpaced its ability to maintain compliance-grade KYC hygiene.

Transaction Monitoring Gaps

- Weak detection of unusual transaction patterns across wallets and linked accounts.

- Potential commingling of funds between merchant and personal accounts.

- Inadequate systems to flag high-velocity transactions typical of layering or mule activity.

Data Governance and Regulatory Reporting

- Concerns over data access, storage outside prescribed parameters, and insufficient internal segregation between Paytm Payments Bank and its parent ecosystem.

- Delayed or incomplete regulatory reporting is hindering supervisory visibility.

These combined lapses exposed a systemic risk, that even a compliant front-end could hide deep-rooted deficiencies in core AML and governance frameworks.

RBI’s Enforcement & Legal Basis

The RBI’s actions were rooted in its powers under:

- Section 35A of the Banking Regulation Act, 1949

- Section 17 of the Payment and Settlement Systems Act, 2007

- Master Direction on KYC (Updated 2023)

- Master Circular on Cyber Security Framework for Banks

Regulatory Timeline

| Year | Regulatory Event |

| 2018 | Early caution notices on KYC standardization |

| 2021 | Transaction data audit ordered |

| 2022 | Ban on onboarding new customers due to “supervisory concerns” |

| 2023 | Data governance and ownership scrutiny intensified |

| 2024 | Final directive restricting operations and account activity |

RBI’s 2024 directive explicitly cited “persistent non-compliance with regulations and continued material supervisory concerns.”

While the move was seen as unprecedented, it reflected the central bank’s increasing emphasis on sustained compliance maturity rather than reactive remediation.

The Regulatory Message: Compliance as Core Infrastructure

The RBI’s approach to PPBL’s case marks a shift from corrective supervision to preventive enforcement, signaling that compliance lapses in core financial infrastructure can trigger swift operational restrictions.

This sets a precedent not only for payment banks but for the entire fintech ecosystem, where speed-to-market often outpaces compliance rigor.

The underlying message: every fintech must operate as a regulated financial institution first, and a technology company second.

The Broader Compliance Context

FATF and FIU-IND Alignment

Globally, the FATF has identified payments and fintech entities as emerging AML hotspots due to:

- High transaction volumes with low per-ticket value.

- Digital onboarding and limited face-to-face verification.

- Cross-platform integration with limited centralized oversight.

In India, FIU-IND mandates that all regulated entities, including Payment Banks, comply with PMLA reporting obligations, Suspicious Transaction Reports (STRs), and threshold monitoring.

Industry-Wide Impact

Following the Paytm Payments Bank order, several fintechs began tightening KYC, revising data-sharing agreements, and strengthening ongoing due diligence.

The case effectively redefined what “good compliance” looks like in fintech, continuous, data-driven, and regulator-ready.

Systemic Lessons for the Fintech Industry

| Dimension | Observed Weakness | Strategic Lesson |

| KYC/CDD | Rapid digital onboarding with incomplete verification | Continuous identity assurance via AI-driven validation |

| Transaction Monitoring | Weak anomaly detection | Real-time pattern analytics and AI velocity scoring |

| Data Governance | Shared infrastructure risks | Segregation of data environments and access control |

| Regulatory Engagement | Reactive remediation | Continuous compliance communication and reporting |

| AML/CFT Oversight | Fragmented monitoring systems | Unified compliance architecture integrated with operations |

The takeaway: fintechs can no longer treat compliance as an auxiliary process — it is the architecture on which trust, access, and scalability depend.

How IDYC360 Prevents & Detects Similar Risks

The Paytm Payments Bank episode illustrates exactly why fintechs need a compliance intelligence layer that keeps pace with their growth.

IDYC360 provides modular, AI-enabled solutions spanning onboarding, monitoring, and governance.

AI-Powered KYC and Ongoing Due Diligence

- Automated document, biometric, and behavioural verification ensures each user’s identity is validated at onboarding and refreshed periodically.

- Deduplication algorithms flag duplicate accounts, false identities, or PEP linkages instantly.

- Continuous KYC ensures data integrity for millions of users, without slowing down onboarding.

Transaction & Behavioural Analytics

- Machine-learning models analyze velocity, frequency, and transaction clusters in real time.

- AI detects patterns typical of layering, mule networks, or round-tripping.

- Cross-platform transaction correlation identifies risk exposure across multiple wallets, merchants, and accounts.

Data Governance and Audit Control

- Centralized data lake architecture with role-based access control (RBAC) and immutability logs for audit trails.

- Compliance-grade evidence storage aligned with RBI and FIU-IND inspection requirements.

- End-to-end encryption and data localization ensure zero regulatory friction on privacy obligations.

Regulatory Reporting and Case Management

- Auto-generation of Suspicious Transaction Reports (STRs) and Cash Transaction Reports (CTRs) for FIU-IND submission.

- Built-in case workflow allows analysts to document alerts, attach evidence, and close compliance cases with full traceability.

Continuous Risk Scoring

- Risk scores update dynamically based on behavioural data and external intelligence feeds.

- Entities linked to high-risk activities or sanctioned jurisdictions are immediately flagged.

- Provides a 360° view of customer risk, enabling fintechs to act before regulatory action becomes necessary.

Fintech-Specific Challenges in Compliance Implementation

Speed vs. Control

Fintechs thrive on seamless user journeys. However, frictionless onboarding often compromises verification rigor.

IDYC360’s APIs integrate seamlessly into digital flows, ensuring compliance without breaking UX.

Third-Party Dependencies

Multiple vendors, PSPs, and aggregators create fragmented compliance responsibility.

IDYC360 consolidates third-party data streams into a single compliance command center, eliminating oversight blind spots.

Scale and Velocity

High-frequency, low-value transactions generate vast data volume.

IDYC360’s AI-driven analytics engine filters noise and highlights truly anomalous patterns, ensuring operational efficiency.

Global Expansion

Fintechs operating across jurisdictions face divergent AML rules.

IDYC360’s compliance modules adapt to both RBI and FATF frameworks, supporting scalable multi-market readiness.

The New Era of Compliance Intelligence

The Paytm Payments Bank case marks a turning point for Indian fintech regulation, moving from compliance checklists to real-time regulatory readiness.

Key trends shaping the next phase:

- Continuous Supervision: Regulators now expect 24/7 data visibility, not quarterly reports.

- Embedded RegTech: Compliance tools must be integrated into core fintech architecture.

- AI-Enhanced Audits: Automated audit trails and behavioural risk models will become standard.

- Data Accountability: Institutions must demonstrate where, how, and why every customer’s data is processed.

IDYC360’s compliance intelligence architecture directly enables this transformation, offering predictive visibility rather than post-event control.

The Broader Regulatory Message

RBI’s enforcement against PPBL was not merely punitive; it was preventive.

The central bank sought to send a systemic message: financial innovation cannot outpace regulatory integrity.

This mirrors global trends. Regulators from MAS (Singapore) to FCA (UK) are increasingly converging on the same principle, “same activity, same risk, same regulation.”

For Indian fintechs, this means compliance excellence will become a competitive advantage.

Institutions that proactively deploy intelligence-driven compliance infrastructure will be best positioned to maintain customer trust and regulatory goodwill.

How IDYC360 Redefines Compliance for Fintechs

| Capability | Compliance Gap Solved |

| AI KYC/CDD Engine | Detects duplication, false identities, incomplete verification |

| Transaction Monitoring | Flags high-velocity and layered transfers instantly |

| Risk Scoring & Alerts | Provides dynamic exposure assessment |

| Beneficial Ownership Graphs | Uncovers indirect control and third-party influence |

| Case Management | Creates regulator-ready audit trails |

| Data Governance Suite | Ensures data privacy, localization, and role-based access |

The outcome is not just compliance; it’s confidence.

Fintechs using IDYC360 can scale operations while remaining regulator-aligned, audit-ready, and customer-trustworthy.

Strategic Takeaways

- Compliance must evolve with business models: Fintechs cannot apply legacy controls to real-time ecosystems.

- Regulatory visibility is now digital: Supervisors expect evidence of compliance, not promises.

- AI is a compliance infrastructure: Intelligent systems can process data volume and complexity that no human team can match.

- RegTech collaboration is the new frontier: Platforms like IDYC360 don’t replace compliance teams; they amplify them.

Conclusion

The RBI’s action against Paytm Payments Bank is more than a regulatory milestone; it’s a signal of transformation.

Fintechs are now expected to build compliance resilience equivalent to traditional banks, supported by technology that provides precision, scalability, and transparency.

This shift is not punitive; it’s protective.

By enforcing accountability, the RBI ensures that India’s fintech revolution remains sustainable and trusted.

For fintechs, the path forward is clear:

“Adopt intelligence-led compliance systems that evolve in real time, align with global AML/CFT norms, and withstand regulatory scrutiny.”

IDYC360 leads this evolution, enabling fintechs to monitor risk continuously, verify identities intelligently, and demonstrate compliance proactively.

In a world where compliance defines credibility, IDYC360 empowers digital institutions to grow securely, compliantly, and confidently.

References

- Reserve Bank of India – Press Release on Paytm Payments Bank restrictions, January 2024.

- Financial Intelligence Unit – Reporting Obligations under PMLA for Payment Banks.

- FATF – Guidance for a Risk-Based Approach to Virtual Assets and Payment Institutions.

- Economic Times – “RBI directs Paytm Payments Bank to halt operations from February 29, 2024.”

- Mint – “Paytm Bank under scrutiny: RBI cites persistent non-compliance.”

- Moneycontrol – “Inside RBI’s action against Paytm Payments Bank: What went wrong.”

Ready to Stay

Compliant—Without Slowing Down?

Move at crypto speed without losing sight of your regulatory obligations.

With IDYC360, you can scale securely, onboard instantly, and monitor risk in real time—without the friction.