Introduction

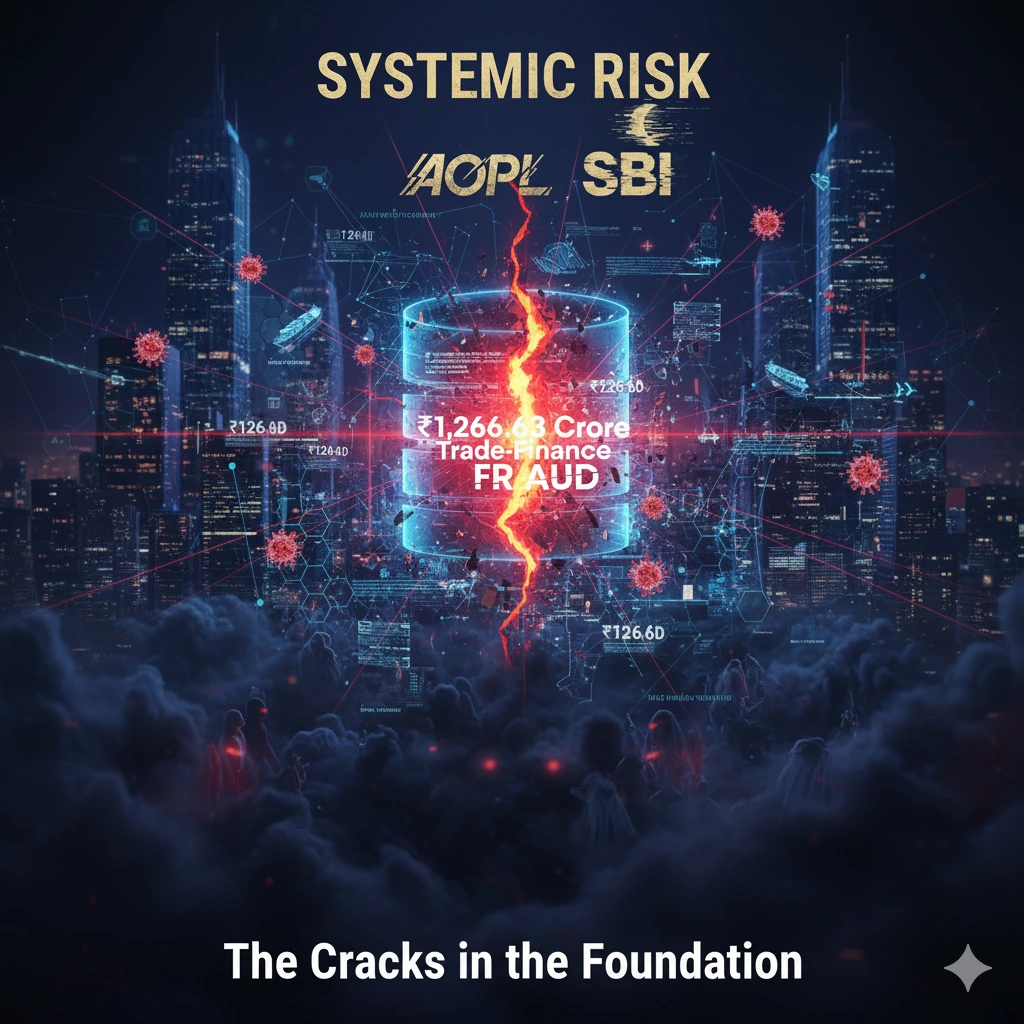

The Enforcement Directorate’s recent provisional attachment of nine Dubai properties linked to an alleged ₹1,266.63 crore bank fraud involving Advantage Overseas Pvt. Ltd. (AOPL) highlights a classic and increasingly consequential hybrid of trade-finance abuse, trade-based money-laundering (TBML), and cross-border asset concealment.

Beyond the headline arrests and asset seizures, this case exposes systemic weaknesses in trade-finance governance, beneficial-ownership resolution, and post-payment surveillance, gaps that enterprise RegTech platforms like IDYC360 are purpose-built to address.

This article explains the scheme as reported, extracts the high-value compliance lessons for banks and regulators, and lays out concrete detection and mitigation approaches that map to IDYC360’s EMD Pipeline and FPSM capabilities.

What the Public Record Shows

According to public reporting and ED disclosures, AOPL allegedly obtained and rolled over a series of foreign letters of credit (FLCs) through State Bank of India, creating exposure when LCs devolved.

Proceeds that flowed offshore, reportedly in the region of US$200 million equivalent in FLC exposures, were allegedly layered through domestic and offshore entities and ultimately used to acquire high-value Dubai real estate.

Several Dubai properties were reported to have been gifted to a director’s family member, a common concealment technique.

Law enforcement seized mobile devices, financial records, and property documents as part of the investigation.

Reported typologies include devolved LCs, circular trading/illegal merchanting, fabricated trade documentation, and cross-border layering into real property, a textbook combination of trade-finance exploitation and asset concealment.

How The Scheme Likely Operated (Technical Anatomy)

While investigators continue to establish facts legally, the public narrative and trade-finance mechanics allow a plausible reconstruction of the typology:

LC Origination and Rollover

AOPL secured FLCs to fund imports or to show trade activity.

When margin requirements or collateral were not maintained, the LCs were rolled over or devolved, producing payment obligations for the issuing bank.

False or Inflated Trade Documentation

Imports/exports were allegedly supported by manipulated invoices, bogus bills of lading, and circular trades that created the appearance of legitimate commerce while extracting value.

Downstream Layering

Bank payments to beneficiary accounts were routed through networks of related parties and offshore intermediaries, fragmenting the transactional trail.

Asset Conversion and Concealment

Funds were converted into immovable property abroad, then transferred into relatives’ names using gift deeds or nominee structures to hide beneficial ownership.

Temporal Coordination

Transfers into property purchases clustered around devolved LC events, suggesting a link between on-book losses and rapid offshore asset acquisition.

This multi-stage process, placement (devolved LC payments), layering (cross-border routing and circular trades), and integration (real estate purchases and gifts), is consistent with sophisticated TBML and fraud schemes.

Why Traditional Controls Often Miss This Pattern

Several institutional tendencies make such schemes hard to detect early:

Siloed Trade-Finance and Transaction Monitoring

Banks frequently treat trade-finance messages (LCs, bills) as separate from payments and customer-transaction streams, limiting real-time correlation.

Insufficient Document Verification

Manual or periodic verification of trade documents fails against large volumes and sophisticated falsification.

Weak Related-Party and UBO Resolution

Nominee ownership, gifting, and rapid transfers to relatives defeat simplistic beneficial-owner models.

Branch-Level Exceptioning and Collusion Risk

Concentrated LC exposures at a single branch, coupled with staff exceptions, can enable abuse.

Cross-Sector Data Gaps

Property registries, corporate registries, and trade data live in different custody models and are rarely fused into a single investigative view.

To detect the AOPL pattern, institutions need cross-domain correlation and rapid pattern-matching across thousands of events, precisely the environment where advanced RegTech delivers value.

Detection and Mitigation: An IDYC360 Playbook

IDYC360’s architecture, the EMD Pipeline, and the Fraud Pattern Speed Matching (FPSM) algorithm are designed to correlate high-velocity events across domains, surface emergent patterns, and deliver prosecutor-grade case artifacts.

Below are practical detection controls and workflows that map directly to the platform’s capabilities.

Real-Time LC-to-Payment Correlation

Ingest LC issuance, amendment, and rollover messages (MT700/701-style metadata or local equivalents) and correlate them with the downstream payment rails.

Flag rapid devolutions followed by immediate offshore beneficiary crediting and subsequent high-value outward transfers.

Establish thresholds for repeated rollover frequency combined with declining margin replenishment.

2. Trade Document Consistency Models

Apply machine-learning document matching to compare invoice line items, HS codes, port-to-port transit times, and bill-of-lading metadata against expected norms for the commodity and corridor.

Detect anomalies such as over-invoicing, mismatched weights, or reused vessel identifiers that suggest circular trading.

3. Related-Party and Gift-Deed Detection

Fuse corporate-registry and property-registry data where available to identify gift deed patterns, nominee ownership, and sudden transfers to kin.

Automated UBO resolution, enriched by negative news and PEP screening, helps surface suspicious transfers of high-value assets abroad.

4. Multi-Node Pattern Matching (FPSM)

Use FPSM to spot emergent network patterns: clusters of entities receiving LC proceeds, fast downstream disbursements to a small set of offshore nodes, and then property purchases in one jurisdiction.

FPSM excels at matching temporal sequences across many entities and data types with minimal latency.

5. Branch and Staff Anomaly Scoring

Combine exception logs, authorization trails, and staff behavior analytics to detect unusual approval patterns, heavy exceptioning for a counterparty, or repeated overrides.

Elevated scores should trigger independent branch audits and escalation to compliance committees.

6. Automated Case Packs for Enforcement

When pattern thresholds are met, auto-generate a consolidated investigative pack: timeline of LC events, payment flows, entity graph, related property registry results, and document consistency scores.

These packs accelerate enforcement referrals and support provisional attachments.

Regulatory & Operational Recommendations

For banks, fintechs, and regulators seeking immediate steps:

Integrate trade-finance metadata into transaction monitoring fabrics

LCs are not isolated commercial documents; they are financial instruments that must feed AML/CFT analytics.

Mandate more frequent, automated trade-document validation

Regulate TBML controls for high-value import/export corridors.

Require enhanced due diligence for high-volume LC counterparties

Ensure UBO transparency and periodic reassessment.

Standardize cross-sector information sharing

Property registries, customs data, and corporate registries must be made queryable for FIUs and designated reporting entities under legal frameworks.

Adopt AI-driven correlation platforms with human-in-the-loop review

Reduce false positives through contextualized alerts and rapid investigative outputs.

Conclusion

The reported AOPL-SBI case serves as a cautionary example of how trade finance, when leveraged with falsified documentation and cross-border layering, can result in catastrophic banking losses and obscure the movement of illicit proceeds into offshore real estate.

From a systemic viewpoint, the remedy is not a single control but a reorientation: Fuse trade-finance messaging, payment flows, corporate and property registers; apply behavior-driven detection; and deliver concise, actionable intelligence to investigators.

For institutions committed to closing these gaps, IDYC360’s EMD Pipeline and FPSM provide the technical scaffolding to detect multi-node TBML patterns, resolve beneficial ownership questions more efficiently, and produce evidentiary case packs that convert alerts into enforceable action.

In an era where financial crime frequently blends corporate structures, professional facilitation, and trade complexity, the speed and breadth of detection matter as much as analytical depth.

References

- Moneylife — “₹1,266 Crore SBI Bank Fraud: ED Seizes Dubai Luxury Assets Gifted by AOPL Chief Shrikant Bhasi to Daughter.”

- Times of India — “ED Attaches 9 Luxury Dubai Properties Worth ₹51.7 Cr; Linked to ₹1266 Cr Bank Fraud.”

- ThePrint — “ED Attaches Nine Luxury Dubai Assets in ₹1,266 Crore SBI Fraud Case Involving AOPL.”

- Business Standard — “ED Attaches Nine UAE Luxury Properties in ₹1,266 Cr SBI Fraud Case.”

- New Indian Express — “Nine Luxury Properties in Dubai Attached by ED in ₹1,266.63 Crore Madhya Pradesh Bank Fraud Case.”

Ready to Stay

Compliant—Without Slowing Down?

Move at crypto speed without losing sight of your regulatory obligations.

With IDYC360, you can scale securely, onboard instantly, and monitor risk in real time—without the friction.